Recent News

International Renewable Energy Agency: The electricity costs of renewable energy + energy storage projects are lower than those of fossil fuels, marking a new stage in the energy transition.From the “Industrial Acceleration Act” to the Inverter Ban: Is Energy Storage the Next Target for the EU?Dai Chu Shou Chao Yu Chu Shou: Risks and Opportunities in the German Energy Storage MarketLatest news on international energy storage as of AprilBeyond the short-term disruptions caused by geopolitical conflicts: The entry rules reshape the core logic of China’s energy storage exports.

Dai Chu Shou Chao Yu Chu Shou: Risks and Opportunities in the German Energy Storage Market

April 20, 2026 NewsOver the past decade, Germany has been one of the most aggressive test beds for global energy transition. From accelerating coal phase-out and completely phasing out nuclear power, to making large-scale bets on wind power and solar power, Germany's power system has been advancing towards a low-carbon future while also facing unprecedented volatility pressure. Price fluctuations in electricity have widened, and negative electricity prices have occurred frequently. Against this backdrop, energy storage is no longer an optional choice but an important flexible regulation resource for maintaining the stable operation of the system. Large-scale battery energy storage has thus moved to the center of the system.

Market situation: German major storage facilities are witnessing a historic turning point

The structure of the German energy storage market is undergoing significant changes.

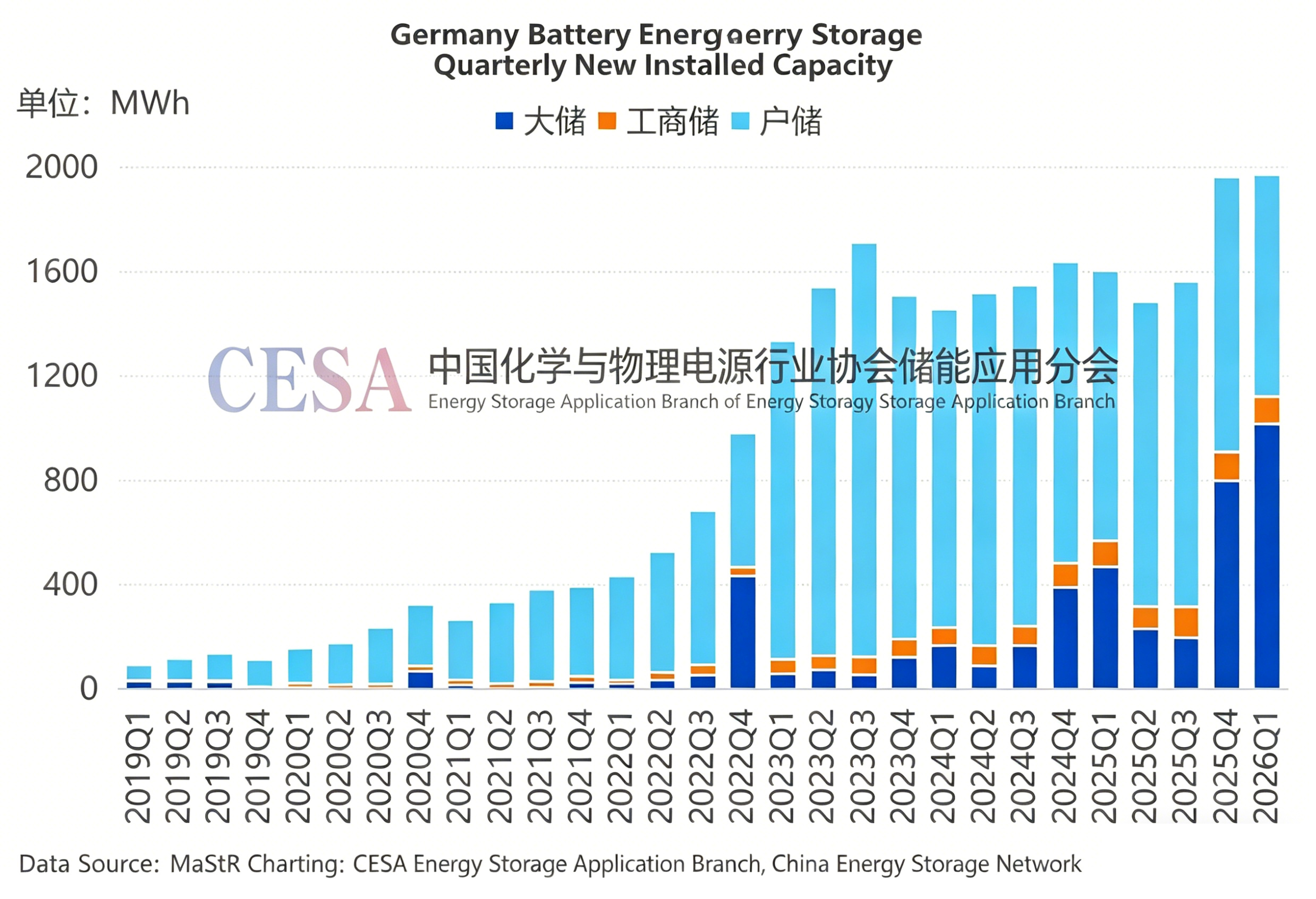

According to MaStR data, as of the end of March 2026, the cumulative installed capacity of battery storage in Germany reached 17.9 GW/27.2 GWh. In the first quarter of 2026, Germany added 1.1 GW/1.97 GWh of new battery storage capacity, with a year-on-year growth of 6.3% (in terms of power) / 23% (in terms of capacity).

The more significant change lies not in the total amount, but in the structure.

The installed capacity of residential storage continued to decline. In the first quarter of 2026, the new installed capacity of residential storage was 569 MW/850 MWh, a year-on-year decrease of -19.9% (power) / -17.8% (capacity), continuing the previous contraction trend. Although industrial and commercial energy storage maintained growth, the scale remained limited, with only an additional 57 MW/108 MWh.

The true turning point comes from Big Storage.

At the same time, the installed capacity of large-scale storage increased by 472 MW/1016 MWh, a year-on-year increase of 72.5% (in terms of power) / 116.2% (in terms of capacity). It exceeded 1 GWh for the first time in a single quarter, and the capacity scale has surpassed that of household storage for the first time in seven years. This change indicates that the focus of the German energy storage market is shifting from distributed to centralized.

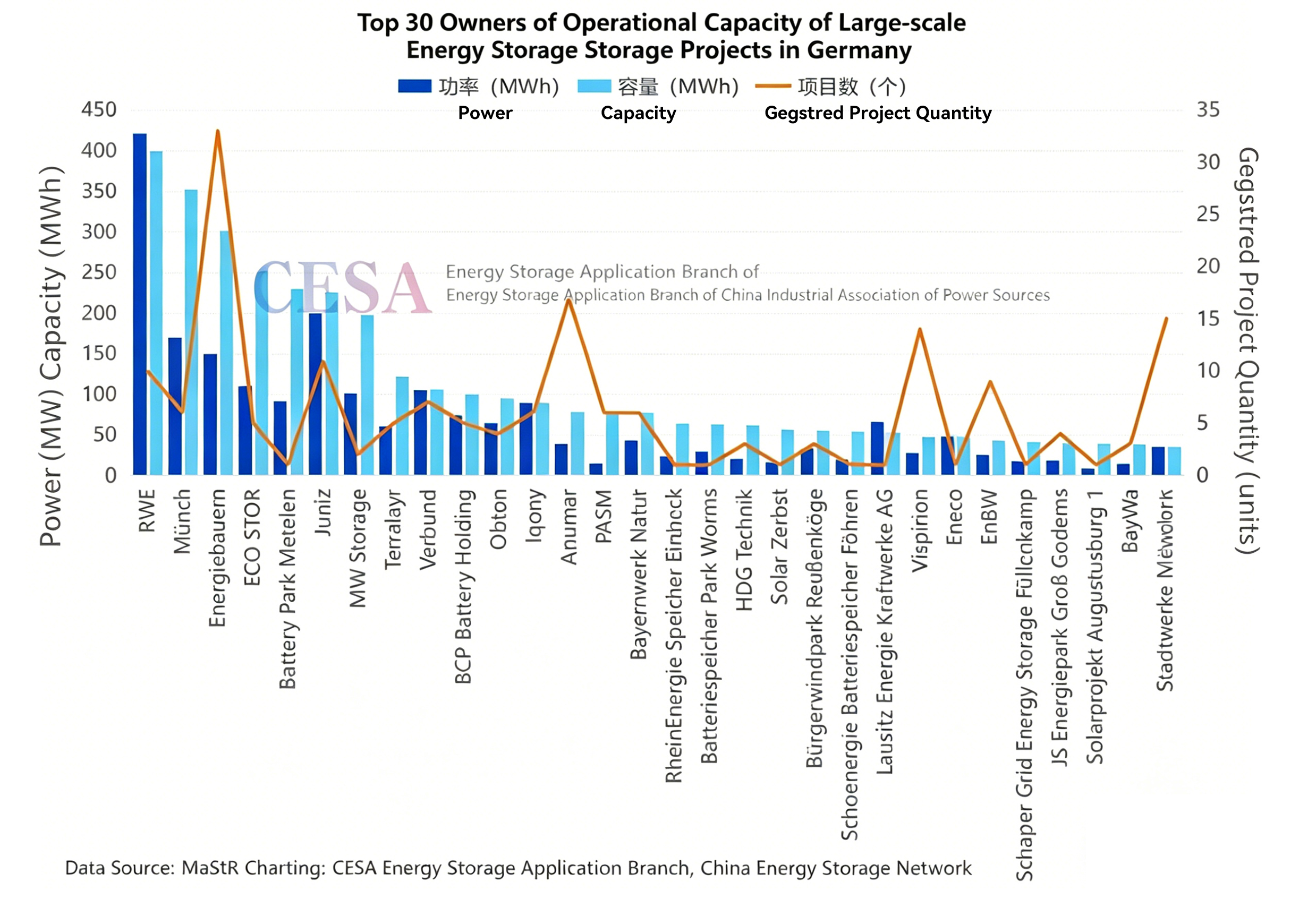

Further analysis shows that as of the beginning of April 2026, the cumulative installed capacity of large-scale storage in Germany has reached 3.17 GW/5.07 GWh, mainly concentrated in several federal states such as Bavaria, North Rhine-Westphalia, Saxony, Thuringia, Saxony-Anhalt, and Schleswig-Holstein.

From the perspective of the project owners of large-scale storage projects, the top 10 constructors have all an operational capacity exceeding 100 MWh. Among them, RWE has the highest capacity, with the cumulative scale of its 10 operational large-scale storage projects reaching 422 MW/401 MWh. Münch and Energiebauern also have operational large-scale storage projects exceeding 100 MW/300 MWh. What is worth noting is that Energiebauern has the most operational large-scale storage projects, with a total of 33 projects.

If the operational projects reflect the current situation, then the planning projects reveal the future trends.

As of the beginning of April 2026, a total of 418 large-scale storage planning projects in Germany have been registered, with a total capacity of 7.06 GW/16.55 GWh. From the perspective of the project owners, the number of capital-oriented energy developers accounts for a significant proportion, and the planned capacity of the top 15 owners exceeds 50 MW/100 MWh.

Among them, LEAG Clean Energy Company plans to build 4 large-scale storage projects, with a total scale of up to 1.6 GW/6.137 GWh, ranking first. ECO Energy Storage Company, East Energy, and Kyon respectively rank second, third, and fourth. Anumar has the most registered large-scale storage planning projects, with a total of 68 projects and a total scale of 188 MW/375 MWh, ranking fifth.

Driving factor: Energy transition boosts demand for flexibility

The sudden surge in Germany's energy storage demand is primarily due to the pressure from macro-level energy security and structural transformation.

The 2022 conflict between Russia and Ukraine had a systemic impact on the European energy system. Germany, a major industrial country in the EU that is highly dependent on external energy, was the first to bear the brunt of the impact. The EU promptly launched the "Renewable Energy Power Plan" (REPowerEU), aiming to break free from reliance on Russian fossil fuel imports, transition to clean energy, and stabilize energy prices.

Germany has even set ambitious energy transition goals through the "Renewable Energy Law" (EEG): by 2030, the cumulative installed capacity of photovoltaic power plants will reach 215 GW, the cumulative installed capacity of onshore wind power plants will be 115 GW, the cumulative installed capacity of offshore wind power plants will be 30 GW, and the proportion of renewable energy in electricity consumption will be at least 80%.

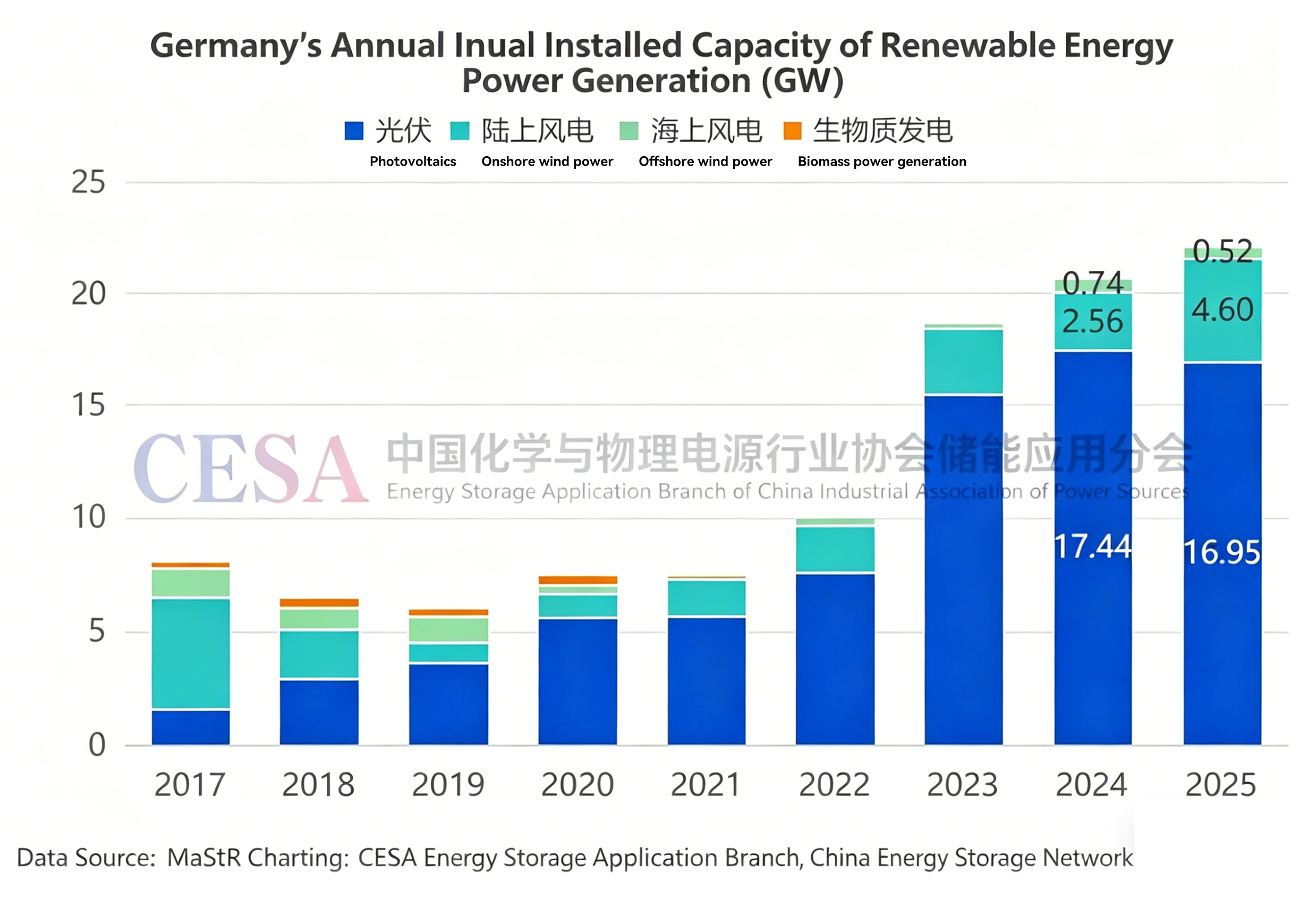

Since 2023, Germany has gradually phased out nuclear power and the installation of renewable energy sources has entered an acceleration phase, with an average annual growth rate exceeding 34%. Data from the German Federal Network Agency shows that in 2025, Germany's installed renewable energy capacity will reach 22.1 GW, an increase of +6.1% compared to the previous year. Among this, photovoltaic power will be 16.9 GW and onshore wind power will be 4.6 GW.

By the end of 2025, the installed capacity of renewable energy in Germany has exceeded 200 GW, among which photovoltaic power is 117.6 GW, onshore wind power is 68.1 GW, and offshore wind power is 9.7 GW. Based on the existing base, when comparing with the target for 2030, it is estimated that the average annual new installation of renewable energy in the period from 2026 to 2030 needs to increase to approximately 33 GW.

In terms of power generation, according to data from the German Federal Statistical Office, the share of renewable energy in Germany's total power generation exceeded 50% for the first time in 2023. In 2025, the total renewable energy generation in Germany was 290 TWh, accounting for 57.2% of the total power generation, remaining largely the same as in 2024. The photovoltaic power generation exceeded the coal power generation for the first time.

As the proportion of renewable energy in power generation has been increasing year by year, coupled with higher installed capacity targets, the demand for flexibility regulation and real-time balancing capabilities in the German power system has significantly increased.

As a flexible resource, energy storage thus becomes a key variable.

The German Solar Association (BSW-Solar) has called for the German government to set legislative targets to achieve at least 100 GWh of battery storage capacity by 2030. This figure actually represents a response to the "flexibility deficit" in the power system.

Meanwhile, negative electricity prices have become increasingly frequent. In 2025, the duration of negative prices in the German day-ahead market reached 575 hours, setting a new record and far exceeding the historical record of 459 hours in 2024. The drastic price fluctuations have provided considerable profit opportunities for energy storage to participate in energy arbitrage and ancillary services.

Revenue change: One-time frequency modulation saturation, day-ahead price spread expands

At the business model level, German energy storage is undergoing a profound reconfiguration.

In the past, frequency modulation (FCR) was the dominant method. However, as the number of participants increased, the market has now shown clear signs of saturation. The focus of profits is beginning to shift.

On one hand, the participation of battery energy storage in secondary frequency regulation (aFRR) has been continuously increasing. For operators that can strategically participate, secondary frequency regulation has become an important revenue source in the German market. On the other hand, energy arbitrage has become the "main battlefield" for the revenue of battery energy storage in Germany.

The German intraday market is one of the most liquid and volatile markets in Europe, with approximately 15% - 20% of electricity transactions taking place here. The intraday market is mainly divided into two trading forms: one is multiple intraday auctions conducted daily, and the other is the continuous trading mechanism.

According to FfE data, in 2025, the average daily price spread in the German day-ahead market widened again compared to 2024, reaching 130.4 €/MWh. The day-ahead auction concludes at 12 noon every day, and energy storage scheduling can be planned and optimized through algorithms. This arbitrage strategy is becoming increasingly attractive.

Furthermore, starting from January 22, 2026, battery storage has been permitted to participate in the instantaneous reserve capacity market, creating new revenue opportunities for storage.

With the relaxation of the re-scheduling mechanism, German battery storage can provide flexibility and receive compensation during grid congestion, further expanding its revenue sources.

It is worth noting that energy storage operators usually do not rely on a single market. Instead, they combine and configure various revenue sources to enhance overall profits. In the revenue stacking model, the algorithm will immediately determine which market has the highest value and accordingly schedule the battery storage. This also highlights the importance of operational capabilities. When the asset conditions are similar, the difference in scheduling strategies often directly determines the final profit performance.

Facing challenges: Regulatory uncertainty is increasing

Despite its rapid growth and increasingly diverse sources of income, the German energy storage market still faces numerous challenges.

1.Backlog of access approval processes

The current most prominent bottleneck lies in the aspect of grid connection.

Since 2024, Germany has been experiencing a "battery tsunami": The arbitrage opportunity has opened up, and the "first-come, first-served" mechanism has attracted a large number of players to "grab the spot first and then proceed". By the end of 2025, the scale of grid connection applications for large-scale storage has exceeded 720GW, far exceeding actual demand. Many of these applications are speculative and repetitive. A large amount of grid connection resources have been occupied, while projects with actual implementation capabilities have been squeezed. The regulatory authorities have had to intervene to correct the situation.

In December 2025, Germany revised the "Grid Connection Regulations for Power Plants" (KraftNAV), removing large-scale storage from the "power plant queue". Previously, storage with a capacity of 100MW or more was treated as a power generation facility and followed the "first-come, first-served" principle; after the revision, the grid connection of large-scale storage mainly relied on general provisions such as Article 17 of the "Energy Industry Act" (EnWG), and the rules became more flexible.

Subsequently, the four major transmission system operators (TSOs) in Germany introduced a "maturity assessment mechanism", replacing the application time ranking with verifiable indicators of project progress. The first round of assessment was launched in April 2026.

Under the new mechanism, grid connection applications will be uniformly evaluated on a periodic basis. If the demand exceeds the grid capacity, it will be prioritized to be allocated to "more mature" projects, and the access plan and time path will be clearly defined simultaneously. The evaluation indicators include land availability, approval progress, technical plan, grid access design and financing capability, etc., to determine the actual feasibility of project implementation.

Under the old KraftNAV rules, 51GW of large-scale storage projects have already received approval for connection. The remaining projects that have not yet received approval will be uniformly included in the new assessment mechanism for handling. The TSO stated that this mechanism has been proven effective in the UK and Norway, and it helps to improve the efficiency and transparency of distribution.

Even so, the reality remains tense: the demand for grid connection will continue to exceed the grid's capacity for a long time. Therefore, the TSO calls for the introduction of legally binding "technical quotas" to allocate resources according to system needs, allowing all entities to connect in an orderly manner and each to occupy its proper position.

Meanwhile, the German Bundestag has requested the government to submit an integrated grid reform draft by the first quarter of 2026. The draft should standardize and digitize the access process for power generation, electricity consumption, and energy storage projects, in order to cope with the systemic pressure caused by the surge in applications. The related reforms also include "grid traffic lights", shared access, and priority ranking mechanisms. The goal is to complete the legislation by 2027 and avoid grid connection bottlenecks from hindering the energy transition.

2. Uncertainty of the power grid charging mechanism

Apart from the connection issue, the electricity grid charging rules are also a key variable.

Usually, when an energy storage system charges from the grid, it is regarded as a terminal user and is required to pay the grid usage fee; however, when discharging to the grid, no such fees are charged. According to Article 118, Paragraph 6 of the "Energy Industry Law" (EnWG), storage projects put into operation before August 2029 can enjoy a 20-year exemption from grid fees. This policy has become an important support for the current investment boom.

However, the sustainability of this exemption mechanism is now being subject to a re-evaluation.

The German Federal Network Agency is expected to release the framework for the grid charging reform (AgNes) in May or June 2026, marking the entry of flexibility resources such as energy storage into a new round of regulatory adjustment cycle. This reform is not only aimed at energy storage but also involves restructuring the entire grid cost system, redistributing expansion and operation costs, in order to encourage more users to jointly bear the system expenses.

The German Federal Network Agency stated that there is a possibility that the current policy of exempting energy storage costs might be tightened prematurely, and it could even affect assets that have already been put into operation. This undoubtedly increases the uncertainty in battery storage investment.

3. Tightening of external regional regulations

At the same time, the external constraints for the project's implementation are also increasing.

By the end of 2025, battery energy storage systems with a capacity exceeding 1 MWh will be recognized as "priority infrastructure" in non-urban areas and will enjoy certain planning conveniences. However, this policy was subsequently tightened.

At present, only two types of projects still enjoy priority status: one is the energy storage system located in conjunction with renewable energy power generation facilities; the other is independent energy storage with a capacity of 4MW or more, and within 200 meters from a substation or a power plant with a capacity of 50MW or more.

This adjustment is believed to have raised the approval threshold, and it may potentially lead to new land conflicts and planning delays in certain areas.

4. Other Challenges

Apart from the aforementioned issues, Germany's energy storage sector also faces a series of other structural contradictions.

On the one hand, at the policy level, there is a fluctuation in the commitment to renewable energy, while the expansion of natural gas installations is advancing. The overall support path is not stable enough, and policy uncertainty continues to rise.

On the other hand, there is also a discrepancy between regulatory practices and legal definitions. Although the "Energy Industry Law" defines energy storage as "core energy infrastructure", the Supreme Court of the United States ruled in July 2025 that, in cases involving the construction or expansion of grid access lines, energy storage still needs to bear the costs of related grid construction, and is still legally regarded as a terminal user.

Furthermore, the approval rules vary among the different federal states, with inconsistent standards. This has increased the burden on local governments, further prolonging the approval process and making implementation more difficult.

International Cooperation: Chinese Enterprises Accelerate Their Layout

Challenges and opportunities coexist. Although the German energy storage market faces numerous challenges such as grid connection backlog and uncertainty in grid charges, as one of the most dynamic energy storage markets in Europe, Germany remains a crucial "landing point" for Chinese energy storage enterprises to expand their business overseas.

According to the incomplete statistics of the CESA Energy Storage Application Committee based on public information, from January 2025 to the end of March 2026, Chinese enterprises in Germany have won over 4.4 GWh of energy storage orders/cooperative projects. Haisuichuang and Sige New Energy both exceeded 1 GWh, ranking at the top. At the same time, companies such as Sunergy Power, Ningde Time, BYD, Cai Ri Energy, Huitang Energy, Jinko Energy, Tianhe Energy Storage, ATS, Haidun Energy Storage, Guoxuan Gaoke, Zhongxinhang, and Funeng Technology have all achieved varying degrees of business presence in the German market.

Haibo Siasun:

In partnership with LEAG Clean Energy in Germany, a 400MW/1600MWh battery energy storage project is being built in Saxony, Germany. An EPC agreement has been signed, and the system will utilize a 5MWh HyperBlock III system.

In March 2026, it announced a contract for a 40MWh grid-side energy storage project in Welterheim. Simultaneously, it successfully secured an order for the second phase of a 40MWh energy storage project in Gorsdorf, providing a complete set of core equipment and a 15-year full lifecycle operation and maintenance service.

Sigen New Energy:

In March 2026, Sigen New Energy signed an 880MWh large-scale energy storage order with Arausol - Arau Technik GmbH, a German photovoltaic system integrator and project developer.

Simultaneously, Sigen New Energy, in collaboration with Arausol and European distributor Memodo, is building Germany's largest DC-coupled photovoltaic power plant, including an 11.6MW photovoltaic system plus a 20MWh SigenStacks distributed battery energy storage system.

By the end of 2025, an agreement was reached with German planning and project management company Steinhoff & Partner to equip a solar power park in Bekum with a DC-coupled SigenStack energy storage system with a capacity exceeding 100MWh.

Furthermore, Sigen New Energy has also entered into a strategic partnership with EC Power, a manufacturer of BHKW (Gas-fired Combined Heat and Power) units. The two parties plan to integrate BHKW with the modular energy storage systems SigenStor and SigenStack. The solution targets residential, commercial, and industrial scenarios, and can be used to store surplus electricity from BHKWs as well as provide emergency backup power. Sigen New Energy will be responsible for the operation and control of the overall energy management system.

BYD: In June 2025, the 103.5MW/238MWh energy storage power station in Bollingstedt, Germany, officially commenced operation. BYD Energy Storage provided 64 MC Cube energy storage systems for the project. Meanwhile, a second-phase project of similar scale is under accelerated construction in Schuby, Germany.

CATL:

In January 2025, CATL signed a strategic cooperation agreement with DHL Group. DHL, headquartered in Bonn, Germany, is one of the world's largest logistics companies, operating in over 220 countries. CATL will provide advanced liquid-cooled energy storage systems and energy management platforms for DHL's logistics parks worldwide.

Furthermore, CATL's battery factory in Thuringia, Germany, with a planned total investment of approximately €1.8 billion and a planned capacity of 14 GWh, is already partially operational and is one of its earliest overseas production bases.

Trina Solar: Trina Solar has partnered with several developers, including Obton and Aquila, signing multiple energy storage project orders. It provides energy storage systems and overall solutions for projects such as Tangermünde (35 MWh), Strübbel (50 MW/100 MWh), and Wetzen (56 MW/112 MWh) in Germany.

Sungrow Power Supply: Signed a supply agreement with Nofar Energy for a 116.5MW/230MWh Battery Energy Storage System (BESS) project in Stendal, Saxony-Anhalt, Germany.

Svolt Energy: In May 2025, it launched a 700MWh large-scale energy storage and commercial/industrial energy storage project in conjunction with innovative German developers and industrial capital, forming a full-chain cooperation model of "development-capital-equipment".

Zinc Energy: Since 2025, it has delivered approximately 220MWh of energy storage systems to Germany.

Jinko Solar: Securing over 200MWh of photovoltaic and energy storage orders in Germany in 2025.

Yuneng Magic Cube: In March 2026, it signed a cooperation agreement with a German partner to provide integrated grid-scale energy storage solutions and complete energy storage system equipment for two projects in Germany, totaling 140MWh, with delivery and grid connection expected by the end of 2026.

Canadian Solar: In November 2025, it signed an energy storage system supply agreement and a 20-year Long-Term Service Agreement (LTSA) for a 20.7MW/56MWh energy storage project in Lower Saxony, Germany. Canadian Solar will provide the SolBank large-scale energy storage system solution for the project, with delivery expected to begin in March 2026.

Haichen Energy Storage: It reached a cooperation agreement with Schoenergie, a German integrated sustainable energy service provider, to officially launch a 21MW/55MWh energy storage project in Germany. Haichen Energy Storage will supply 11 5MWh energy storage containers.

Furthermore, CATL, Zhongchuang Aviation, Guoxuan High-Tech, and Farasis Energy have all invested in and built battery production bases in Germany, with a planned total capacity of 64GWh, further strengthening their localized supply capabilities.

Overall, from solution provision and EPC contracting to localized production and operation, Chinese companies are cultivating the German energy storage market in their own unique ways, actively contributing to its energy transition and making a Chinese contribution to a clean, efficient, and sustainable energy future.

Future Outlook: Policy Evolution Enhances Energy Storage Value

The ambitious energy targets, the continuous expansion of renewable energy, the increasing price fluctuations, and the simultaneous rise in flexibility demands have jointly formed the foundation for the long-term growth of battery storage in Germany.

MiSpeL (Mid-2026)

In the middle of 2026, the Integrated Regulatory Framework for Energy Storage and Charging Facilities (MiSpeL) will be officially implemented.

In the past, Germany mainly supported shared-site energy storage through "innovation tenders". However, the mechanism was severely constrained: if battery storage was to receive cost reduction or subsidies, it could only draw power from the shared-site renewable energy sources and was prohibited from drawing power from the grid. As a result, the profit margin for energy storage was compressed, and paths such as wholesale arbitrage, multi-market optimization, and auxiliary services were restricted. Developers were forced to make a choice: either opt for the subsidy model, with limited returns; or switch to a fully market-based approach, with higher risks.

The core change of MiSpeL lies in relaxing this constraint. Under the condition of meeting the requirements, co-located energy storage can simultaneously charge with renewable energy and grid power, and still retain the eligibility for EEG subsidies. This will fundamentally reshape the operation model and revenue structure of co-located energy storage in Germany. By introducing diversified business paths, the project can flexibly switch between different markets and achieve bidirectional charging, thereby obtaining incremental revenue in multiple markets.

EEG 2027 (Expected to come into effect in 2027)

Meanwhile, the renewable energy subsidy system in Germany is also undergoing accelerated restructuring.

The EU's approval of state aid for Germany's "Renewable Energy Act" (EEG 2023) will officially expire on December 31, 2026. This law is the core subsidy framework for Germany's support of renewable energy power generation.

In February 2026, the draft of Germany's "Renewable Energy Act 2027" (EEG 2027) was leaked. The document was dated January 22, 2026 and is currently in the stage of cross-departmental review. The most significant changes in this draft include: introducing a two-way differential contract mechanism, eliminating the fixed feed-in tariff subsidy for new projects, ceasing support for small projects under 25 kW, and introducing a resilience auction mechanism in accordance with the EU's "Net Zero Industry Act".

Overall, the support mechanism for renewable energy in Germany will shift from unilateral market premiums to a symmetrical difference contract system, closer to the British model. At the same time, it will incorporate dynamic low-price adjustments and flexible exit mechanisms. However, this is still an unpublicized draft and the final version has not yet been implemented. It is scheduled to take effect on January 1, 2027, but this goal is quite challenging.

Once implemented, the German electricity market will gradually shift from a model based on power generation subsidies to one that places greater emphasis on marketization, capacity value and system flexibility. The importance of energy storage will also increase simultaneously.

Capacity market mechanism (will be gradually initiated in 2027 and fully operational by 2032)

As the proportion of fluctuating power sources such as wind and solar energy continues to increase, coal power is accelerating its exit, and the German power system is entering a "high volatility era". The demand for controllable power sources has significantly risen. Against this backdrop, establishing a capacity market mechanism has shifted from an optional measure to a necessary requirement for the system.

Initially, Germany's approach was relatively straightforward: by building new gas power stations, it aimed to fill the power supply gap during periods of "no wind and no sunlight". However, within the framework of the EU's emphasis on the principle of technological neutrality, a compromise solution was eventually formed: before the full implementation of the capacity market, a transitional mechanism was adopted to gradually establish a controllable capacity system.

On January 15, 2026, the German Federal Ministry of Economic Affairs and Energy (BMWE) reached a principle agreement with the European Commission on the power plant strategy. The core framework became increasingly clear: Before the full capacity market is launched in 2032, through approximately 41 GW of transitional tenders, the gap in controllable power sources will be gradually filled.

Among them, the first batch of 12GW tenders will be launched by the end of 2026. 10GW of this will be long-term dispatchable capacity, mainly consisting of hydrogen-compatible gas-fired power plants. Another 2GW is for technology-neutral competition, and energy storage, small-scale units, and aggregated power sources can all participate. The contracted capacity must be put into operation by 2031 at the latest. Subsequent tender plans will be arranged in 2027 and 2029 respectively. The goal is to gradually implement the controllable power generation capacity required by the system by 2031.

For energy storage, this mechanism brings both opportunities and uncertainties. In the transitional bidding process, energy storage can theoretically participate in approximately 31 GW of bids. However, the final winning rate still depends on the yet undefined "reduction coefficient".

Germany plans to establish a comprehensive technology-neutral capacity market framework by around 2027, with the aim of ensuring its full and official operation in 2032.

From the perspective of business model, battery storage can currently achieve positive market-based returns without long-term contracts. However, the introduction of the capacity market may lower peak electricity prices, thereby affecting the arbitrage space of storage. At the same time, the long-term stable cash flow brought by capacity payments will significantly improve the project's leverage structure and financing conditions.

Take the British market as an example. In 2025, the revenue from the capacity market accounted for approximately 10% of the total revenue from energy storage. By the fourth quarter of that year, it had risen to 15%. Against the backdrop of Germany's upcoming grid cost reform, this stable revenue source may become a key support for the financing of energy storage projects.

It should be noted that the relevant agreements have not yet completed the national aid approval process. After the submission of the formal legal draft, further approval from the European Commission is still required. Meanwhile, the specific design of the capacity market is still under continuous discussion, and the final implementation path remains subject to change.

Conclusion: High growth coexists with high complexity

Germany is one of the countries in Europe with the most volatile electricity market, which is highly attractive for energy storage. However, at the same time, the uncertainty of regulation, the diversified revenue structure, have significantly increased the complexity of the industry and raised the professional threshold.

The future competition is not only determined by project acquisition, but also by the depth of understanding of the market mechanism, as well as the ability to optimize cross-market and multi-strategy operations.

Overall, the German energy storage market is still on a rapid upward trajectory. However, this is not an easy path; it is more like a path that combines "high growth" and "high complexity". Challenges and opportunities will coexist in the long term.

During this process, Chinese enterprises are becoming an important participant in Germany's energy transition by providing technological output and implementing localized strategies.

RELATED POSTS

-

Ningbo Jing Hong Energy Technology Co., Ltd.

Room 205, 2nd Floor, Building 3, No. 128,Jingyuan Road, Ningbo High-tech Zone,Zhejiang ProvinceA Tech Power B.V.

VAT ID: NL865234759B01

Grevelingenhout 45, 4311NL, Bruinisse, the Netherlands

©2023 wpboss.cn, wordpress theme designer