Recent News

Has the European battery industry stopped insisting on “local manufacturing”?1390MW! Australia’s Victoria state accelerates approval process for deployment of four energy storage projectsOutlook for the Residential Solar and Energy Storage Market in the United States in 2026The restaurant project completed by JHPVTECH in Tuzkhumahar Town, IraqOutlook for the Energy Storage Market in the First Half of 2026: More Records on the Horizon

Has the European battery industry stopped insisting on “local manufacturing”?

July 6, 2026 NewsAlthough the EU's "Industrial Accelerator Act" proposed in the first half of this year envisioned various scenarios for "European manufacturing" of advanced industrial products, the reality is that once confident European battery startups are increasingly relying on production lines in Asia. The Financial Times of the UK reported on June 29 that recently, several European and American battery companies are negotiating with Chinese manufacturers to lease idle production lines for them to undertake assembly work. Over the past few years, the EU has been hoping to break free from the so-called "China supply chain dependence" by building local super battery factories. The once highly anticipated Swedish company Northvolt (whose Chinese name is "Beifu") was the representative of this strategy. However, due to the poor stability of its multiple "local-based" supply chains, the company declared bankruptcy in 2025. Since then, more and more European and American companies have questioned the need to break away from the Chinese supply chain and independently build a battery industry system.

Willing not to repeat the same fate as the bankruptcies of European giants

According to the Financial Times, taking into account the high manufacturing costs of batteries in Europe, the lengthy project approval process, as well as the impact on market psychology caused by Northvolt's bankruptcy, many European and American battery startups have turned their attention to idle battery production capacity in Asia regions such as China. They hope to achieve rapid mass production by leveraging mature supply chains and manufacturing systems.

One such company is Altris, a Swedish manufacturer of sodium-ion battery materials. The Financial Times reported that the company is in talks with a Chinese battery manufacturer about leasing idle lithium battery production lines, with the plan to transform them and use them for the mass production of energy storage sodium-ion batteries in the future. The CEO of Altris, Krist Bergquist, said that the company is also exploring whether it can utilize other suppliers in Europe that have capacity overcapacity. This approach reflects the changing business model of the European battery industry. Previously, Northvolt attracted investment from various sectors in Germany, including finance and the automotive industry, to build its own factory. However, after expansion, the company faced supply chain instability and product delays, and ultimately went bankrupt.

The online professional website InsideEV recently reported that in the first half of this year, the automotive battery company invested by the multinational automakers Stellantis in Germany and Italy suspended its two battery factory projects. The company stated that the "preconditions" for starting these factories had not been met. German automotive giant Porsche began to reduce the production volume of its Cellforce battery division last year. The reason given by this automaker was that large-scale production (of batteries) "was no longer economically feasible". Such a precedent has prompted a large number of European start-up battery companies to adopt a light-asset operation model.

Similar trends have also emerged in the United States. The American battery startup Ion Storage Systems is currently scouting idle production lines in Southeast Asia to assemble its own batteries and has already connected with over a dozen suppliers. The company claims to have launched a solid-state battery suitable for wearable devices and some industrial niche markets. The company's CEO, Schneider, said that the current competition in the battery powertrain sector is already very intense. In contrast, foundries are more willing to produce specialized batteries for high-profit segments. He stated, "Our core business is a self-developed anode material, and the battery assembly process will be fully outsourced; we will not build a super factory ourselves to avoid repeating the mistakes of Northvolt." Another startup based in California, Unigrid, focuses on the research and development of energy storage sodium-ion batteries. The company plans to adopt a contract manufacturing model and complete component production through six factories located in China, Japan, and South Korea. "Partnering with Asian supply chain enterprises is one way for us to achieve large-scale production of our products," said the company's CEO. Some European startups have stated that relying on the Chinese supply chain support, project implementation is much faster than in Europe; the cumbersome approval process and shortage of skilled workers in Europe remain the core obstacles.

The industry mindset is returning to rationality.

Recently, the German industrial media Springer Professional cited a research report jointly released by the German Machinery Industry Association (VDMA) and other institutions, stating that as the construction boom of "super factories" for batteries in Europe cools down, the mindset of the European battery industry is returning to rationality.

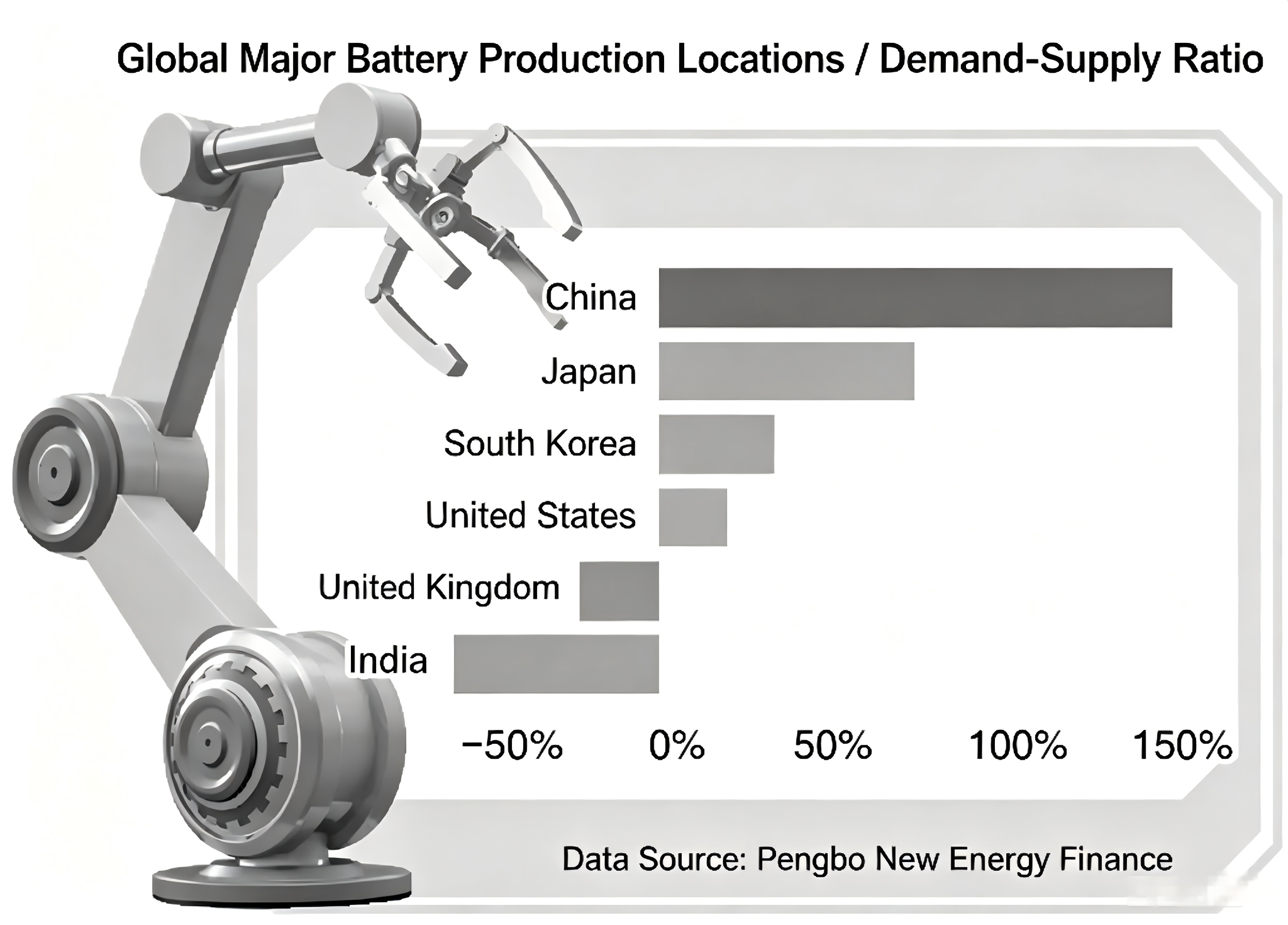

Several German industry insiders in the battery sector told a special reporter from Global Times that the failure of projects such as Northvolt has exposed the real challenges faced by Europe and the United States in the battery manufacturing sector, including high construction costs, difficulties in financing, long approval processes, insufficient industrial chain support, and a lack of experience in large-scale production. This also indirectly confirms the comprehensive competitive advantages of Asia, especially China, in the battery industry chain. After more than a decade of development, China not only has the world's most complete battery industry chain, a mature manufacturing system and abundant engineering and technical talents, but also has achieved cost advantages brought about by scale effects.

According to German reports, in 2025, Germany's battery production increased by 11% compared to the previous year, with the output reaching a new high of 8.1 billion euros. The total value of battery imports for the entire year was 22 billion euros, while exports were 7.8 billion euros. China remains the main supplier to the German market. In 2025, the total amount of batteries imported by Germany from China increased by 25% year-on-year, reaching approximately 11 billion euros. Imports from other European countries decreased by 11%. The general manager of the German Electrical and Digital Industry Association (ZVEI), Gunter Kellermann, stated that these data all indicate the high dependence of the European battery industry on the Asian supply chain.

Yu Qingjiao, the chairman of the Zhongguancun New-Type Battery Innovation Alliance, told the Global Times that currently, the elimination race in the global new energy battery industry has entered a highly intense stage. The industry reshuffle is reshaping the market landscape with an unprecedented intensity. The bankruptcies and reorganizations of former European star enterprises such as Northvolt, as well as the repeated delays and even cancellations of the construction of battery factories by international automakers like Volkswagen and Ford, have all sent a realistic warning to Europe and the United States that they should not attempt to break away from the Chinese supply chain and independently build a battery industry system.

In contrast, China has already established an overwhelming advantage in the fields of batteries, key battery materials, and manufacturing equipment. The global market share of the entire industry has reached as high as 70-80%, and for some core links such as negative electrode materials, they have long held a market share of over 95%. Yu Qingjiao said that the advantages of China's new energy battery industry not only lie in the scale effect, but also are deeply rooted in the collaborative efficiency, process accumulation, and rapid iteration capabilities of the entire industrial chain. Building local battery manufacturing capabilities based on China's complete industrial chain is gradually becoming a realistic and inevitable path choice for the European and American markets. This is not merely based on short-term cost considerations, but is a natural result of the global new energy industry seeking the optimal solution between scale, efficiency, and technological innovation.

Expanding cooperation is the key to reaping the benefits.

Meanwhile, Chinese battery manufacturers are also actively seeking overseas partnerships. According to Springer Professional, a battery company from Wuxi, China, has a global market share of over 20% in lithium battery equipment and supplies to ten battery super factories in Europe. The factory of PowerCo, a battery company under Volkswagen Group, located in Lower Saxony, Germany, is one of its clients.

The Financial Times quoted Rick Lubbe, the CEO of the US battery technology company Group14, as saying that the massive expansion of China's battery production capacity has completely reshaped the profit models of global competing enterprises. He said that the outsourcing behavior of the West might strengthen China's control over key supply chains. "The domestic battery manufacturing capacity in Europe has been continuously shrinking, and car manufacturers have to turn to Chinese suppliers to purchase products."

"Based on the current development of the industry, although there are some voices suggesting that we should 'be cautious' about Chinese products, for European and American battery enterprises, in the absence of a cost base, industrial support, and experience in scale production, it is extremely difficult for them to establish an independent global-competitive industrial chain. The prospects are also worrying." Yu Qingjiao believes that in the coming years, the global battery industry will still heavily rely on China's manufacturing ecosystem. Any attempt to "decouple" must recognize the huge challenges based on this reality. Max Reed, the head of the battery business at consulting firm CRU, said that the Chinese supply chain is still crucial for European battery manufacturing. The "excellent manufacturing capabilities and professional technologies" that the region possesses are becoming increasingly scarce in Europe.

An industry insider told the Global Times that although the attempts of European local super factories have temporarily failed, some European battery enterprises are now entering the stage of selecting technologies for refinement, still expecting to gain an advantage in some new technological fields. Reports from institutions such as VDMA predict that by 2035, the cumulative investment in equipment for battery factories in Europe will reach 250 to 280 billion euros. In response to the advantages of Chinese battery enterprises in the lithium battery industry chain, some European enterprises have begun to focus their attention on sodium-ion batteries. The German "Frankfurter Allgemeine Zeitung" stated that due to the relatively abundant sodium resources in Europe, developing sodium-ion batteries can help Europe reduce its reliance on the Chinese battery industry. However, the report of the International Energy Agency said that "almost all the existing production capacity of new energy batteries in the world" is concentrated in China. Industry data shows that among the planned and constructed sodium-ion battery production capacity before 2030, China accounts for as high as 95%. CATL recently announced that the sodium-ion battery it released a year ago has successfully achieved gigawatt-hour-level large-scale production. Companies like BYD are also actively developing sodium-ion batteries. And Western battery developers have not made as significant progress as China in the mass production of new types of batteries.

Yu Qingjiao further analyzed that for the overseas market, the penetration rate of China's battery material supply chain has been continuously rising and has become an irreversible long-term trend. This is due to the solid foundation that Chinese enterprises have built in resource processing, precursor synthesis, and key material preparation. This advantage is not only reflected in costs, but also in response speed and engineering capabilities. Only by expanding and deepening cooperation with China's battery industry chain can European and American battery enterprises fully enjoy the opportunities and benefits brought by industrial development.

RELATED POSTS

-

Ningbo Jing Hong Energy Technology Co., Ltd.

Room 205, 2nd Floor, Building 3, No. 128,Jingyuan Road, Ningbo High-tech Zone,Zhejiang ProvinceA Tech Power B.V.

VAT ID: NL865234759B01

Grevelingenhout 45, 4311NL, Bruinisse, the Netherlands

©2023 wpboss.cn, wordpress theme designer